The smartphone in your hand, the electric vehicle silently gliding down the street, the massive wind turbines turning rhythmically on the horizon, and the sophisticated defense systems guarding national borders all share a common, hidden bloodline. They are tethered to a handful of elements pulled from the earth, materials that have fundamentally redrawn the geopolitical map of the 21st century. Welcome to the era of the critical mineral rush, a high-stakes economic chess match where the grandmasters are mining conglomerates, nation-states, and tech titans.

At the center of this maelstrom sits cobalt. While technically a transition metal and not chemically classified as a "Rare Earth Element" (REE), cobalt is permanently inextricably linked to rare earths in the global economic narrative. Together, cobalt and true rare earths like neodymium and dysprosium form the indispensable bedrock of the global energy transition. We are no longer fighting over oil fields in the Middle East; the new battlegrounds are the rust-red, mineral-rich soils of the Democratic Republic of Congo (DRC), the high-pressure acid-leach facilities of Indonesia, and the frozen, untapped expanses of Greenland.

As we navigate through 2026, the economics of these minerals have never been more volatile, fascinating, or ruthless. The green revolution has a heavy, metallic price tag, and the race to secure it is reshaping alliances, driving unprecedented technological innovation, and testing the limits of global supply chains.

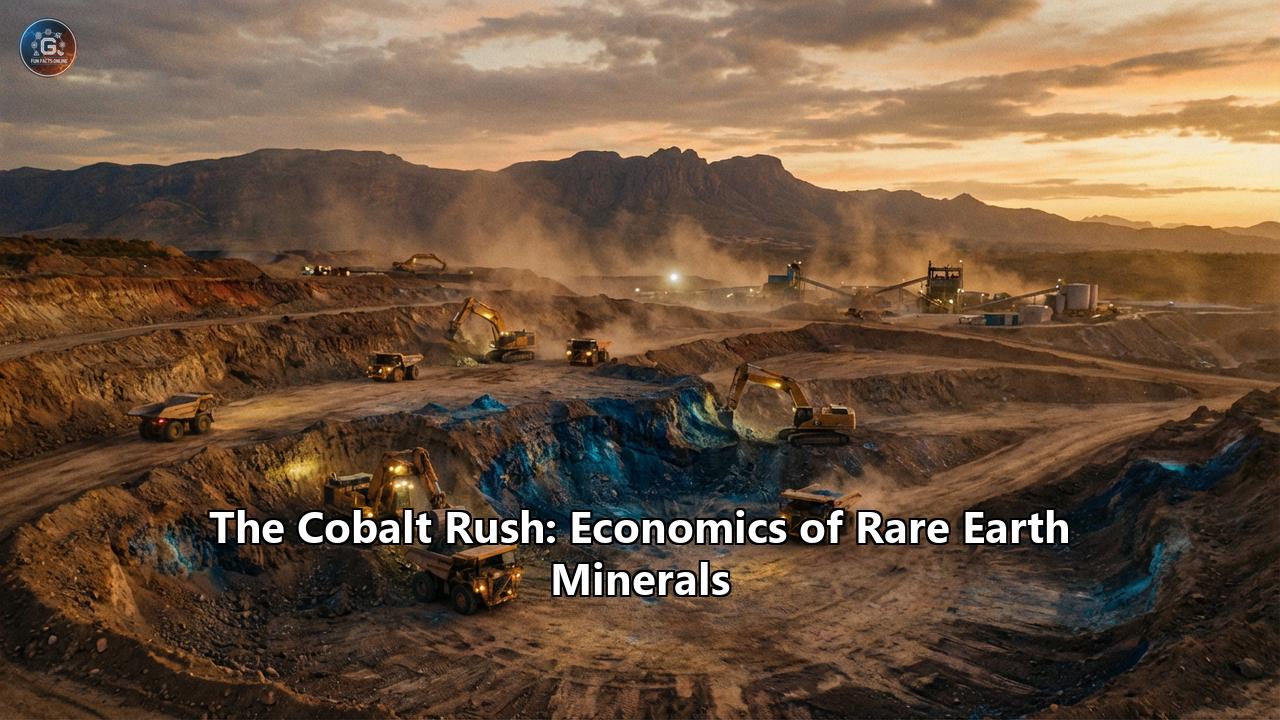

The Anatomy of a Mineral Rush

To understand the economics of cobalt and rare earth minerals, one must first understand their unique utility. Cobalt is the miracle binder of the battery world. In traditional lithium-ion batteries—specifically the Nickel-Manganese-Cobalt (NMC) chemistries that have dominated the consumer electronics and electric vehicle (EV) markets for decades—cobalt acts as a stabilizing agent. It prevents the battery cathode from overheating and degrading, essentially acting as the structural integrity that prevents your laptop or EV from catching fire while allowing it to hold a dense energy charge.

Meanwhile, true rare earth elements (a group of 17 chemically similar elements) are the magical ingredients of modern magnetism. Neodymium and praseodymium are used to create the permanent magnets that translate electrical energy into physical motion. Without them, the motors in electric vehicles would be impractically large and heavy, and the generators in wind turbines would be cripplingly inefficient.

For years, the market for these materials hummed along predictably. But the Paris Agreement, the global push for net-zero emissions, and the explosive mainstream adoption of electric vehicles lit a match under the market. The global cobalt market, valued at roughly $16.96 billion in 2024, is currently projected to surge past $25.91 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.7%. But that steady, annualized growth rate masks a market defined by breathtaking volatility and fierce, bare-knuckle geopolitics.

The Cobalt Rollercoaster: The Price Shocks of 2025–2026

If you want to understand the modern commodity market, look no further than the dramatic price rollercoaster of cobalt between early 2025 and 2026.

In early 2025, the market was actually drowning in supply. Aggressive mining expansions and a temporary surplus sent cobalt prices crashing to a painful $21,000 per tonne. For the Democratic Republic of Congo—which holds a staggering monopoly over the global market, producing upwards of 72% to 76% of the world's mined cobalt—this price collapse was economically unacceptable.

In a flex of pure sovereign power, the DRC government enacted a sudden, full-scale embargo on cobalt exports in February 2025. The goal was simple: starve the market, drain global inventories, and force the price back up to a premium. The embargo sent shockwaves through the global supply chain, particularly hitting China, which relies on the DRC for the vast majority of its unrefined cobalt intermediate products.

By October 2025, the DRC lifted the outright ban but replaced it with a draconian export quota system. Under the new regime, the DRC legally capped its global exports to just 96,000 tonnes for 2026—effectively halving its export volume compared to 2024 production levels. Bureaucratic bottlenecks and delays in implementing the system meant that the first truck carrying cobalt under the new quota rules didn't even leave the country until January 2026.

The economic fallout was immediate and violent. Refiners in China, who had been surviving by draining domestic inventories at the Wuxi Stainless Steel Exchange, suddenly found their stockpiles depleted by nearly 40%. Panic buying ensued. By early 2026, the price of refined cobalt on the London Metal Exchange had more than doubled, violently rebounding to over $48,750 a tonne, with market forecasts predicting an average price of $55,150 a tonne throughout the year.

This price shock sent a crystal-clear message to the world: the era of cheap, unquestioned access to critical battery metals was officially over.

The "Sovereign Free Agent" and the Death of the Global South

The DRC's aggressive market manipulation highlights a profound geopolitical shift that defined late 2025 and early 2026. For decades, geopolitical analysts categorized developing resource-rich nations under the umbrella of the "Global South"—a supposed unified bloc standing in solidarity against Western hegemony. But the cobalt rush has proven that in the critical minerals market, solidarity is dead. It has been replaced by the era of the "Sovereign Free Agent".

The DRC is playing a masterful, highly transactional game. Historically, Chinese state-backed companies have dominated the Congolese mining sector, controlling between 70% and 80% of the country's cobalt output. The DRC also remains heavily indebted to Chinese creditors, owing upwards of $24 billion. In the old world order, this would make the DRC a captive vassal state to Beijing.

But in the new critical mineral economy, the DRC is simultaneously courting the West. In a shocking geopolitical maneuver in late 2025, which was expanded in early 2026, Kinshasa signed a sweeping Strategic Partnership Agreement with Washington. This deal granted American companies preferential access to specifically designated mining assets—a Strategic Asset Reserve (SAR)—worth trillions in cobalt, copper, and lithium.

Simultaneously, the United States, recognizing its dire vulnerability, launched the FORGE initiative in February 2026—a preferential trade zone for critical minerals designed to pull 54 allied and developing nations into a Western-aligned supply chain. The DRC isn't choosing a side in a new Cold War; it is brilliantly auctioning access from both checkout lanes at once, extracting maximum economic value from both Washington and Beijing.

China’s Achilles' Heel: The Refining Chokepoint

While the US scrambles to secure raw mining assets, China holds a different, equally terrifying monopoly: processing and refining. As of 2024, China accounted for a staggering 78% of the world's refined cobalt output. You can mine all the raw cobalt ore you want in Africa or Australia, but before it can be put into an electric vehicle battery, it must be chemically refined into battery-grade cobalt sulfate. And right now, all roads lead to Beijing.

However, the 2025–2026 DRC export quotas exposed China's critical vulnerability. China is a refining superpower, but it is deeply resource-poor when it comes to domestic cobalt reserves. The moment the DRC turned off the tap, Chinese refineries were starved of the raw hydroxide needed to keep the global battery engine running. The "payable" value of Congolese hydroxide—the price refiners must pay relative to the finished metal—surged from 55% to 100%, erasing profit margins and forcing Chinese battery makers into a state of acute crisis.

This dynamic has created a fragile "Mutually Assured Destruction" in the global economics of green energy. The West relies on China for refined batteries, China relies on the DRC for raw minerals, and the DRC relies on global demand to fund its economy. If any one pillar collapses, the entire global energy transition grinds to a halt.

The Human Toll: "Blood Cobalt" and the ESG Reckoning

You cannot discuss the economics of cobalt without confronting its dark, human underbelly. The DRC's vast mineral wealth is inextricably linked to severe human rights abuses, environmental degradation, and modern-day slavery. A significant portion of Congolese cobalt is extracted by "artisanal miners"—a sanitized industry term for hundreds of thousands of impoverished men, women, and children digging by hand in treacherous, unregulated, and structurally unsound pits.

These "blood cobalt" supply chains are notoriously opaque. Artisanal cobalt is frequently smuggled, mixed with industrially mined cobalt, and sold to international refiners, making it nearly impossible for a Western automotive CEO to definitively prove that their flagship electric vehicle is entirely free of child labor.

By 2026, Environmental, Social, and Governance (ESG) mandates have evolved from corporate buzzwords into strict, punitive regulatory frameworks. The European Union and the United States have implemented stringent traceability laws, forcing automakers to audit their entire supply chains. Consequently, a two-tiered economic market has emerged. "Clean" cobalt, mined from strictly regulated, mechanized operations in countries like Australia and Canada, commands a massive premium. However, these alternative hubs simply do not have the volume to displace the DRC.

To bridge the gap, major conglomerates like Glencore—which operates massive, heavily monitored industrial mines in the DRC like Mutanda and Kamoto—are deploying advanced satellite-based analytics, AI carbon footprint monitoring, and blockchain traceability to prove their cobalt is ethically sourced. But the stigma of "blood cobalt" has ultimately triggered an economic reaction far more powerful than any ESG audit: the aggressive technological pivot to engineer cobalt out of the equation entirely.

The Innovation Imperative: Escaping the Cobalt Trap

The highest rule of economics is that necessity breeds innovation. Driven by skyrocketing costs, supply chain bottlenecks, and the PR nightmare of human rights abuses, the global battery industry has embarked on a furious race to eliminate its reliance on cobalt and nickel.

In 2025, a monumental tipping point was reached. For the first time in history, the deployment of low-cost Lithium Iron Phosphate (LFP) batteries officially surpassed traditional nickel-based and cobalt-based (NMC) chemistries in global EV deployments.

LFP batteries use zero cobalt and zero nickel. Instead, they rely on iron and phosphate—materials that are incredibly cheap, abundant, non-toxic, and free from the geopolitical baggage of Central Africa. Historically, LFP batteries were shunned by Western automakers because they had a lower energy density than NMC, meaning shorter driving ranges. But relentless engineering—particularly from Chinese giants like BYD and CATL—has closed the gap. By introducing structural innovations like "cell-to-pack" architectures, engineers have squeezed more LFP cells into the same physical footprint, effectively neutralizing the range anxiety debate.

By late 2025, LFP packs accounted for over 50% of the global EV market, and an overwhelming 80% of EVs sold in China utilized this cobalt-free chemistry. Western automakers, desperate to cut costs and shield themselves from price shocks, are aggressively adopting the technology. Even standard-range models from Tesla and upcoming entry-level EVs from Ford and Volkswagen are abandoning cobalt in favor of LFP.

But the innovation doesn't stop at LFP. As we move deeper into 2026, the battery market is diversifying wildly. Sodium-ion batteries, which replace lithium entirely with cheap, abundant salt, are emerging as the holy grail for stationary grid storage. Solid-state batteries, which replace flammable liquid electrolytes with solid ceramics or polymers, promise to deliver unprecedented energy density and safety for premium, long-range vehicles, though they are still battling manufacturing scalability. Furthermore, innovations like 3D smart electrodes are physically restructuring the internal architecture of batteries to drastically improve conductivity and output without requiring expensive metals.

Does this mean the cobalt market is dead? Far from it. While EV makers are diluting the amount of cobalt per vehicle, the sheer, explosive volume of global EV production means total cobalt demand continues to rise. Furthermore, cobalt is economically irreplaceable in high-end applications. It remains critical for aerospace superalloys (used in jet engines), advanced munitions, 5G hardware, and medical radiotherapy. As the battery market shifts, cobalt is quietly repositioning itself as an elite, high-performance defense and aerospace metal, shielding it from cyclical downturns in the auto sector.

The True Rare Earths: The Greenland Gambit

While the battery industry fights over cobalt, a second, arguably more severe resource war is raging over true Rare Earth Elements (REEs). If cobalt powers the battery, rare earths like neodymium, praseodymium, dysprosium, and terbium power the motor. They are essential for the ultra-strong permanent magnets required in EV drivetrains, offshore wind turbines, F-35 fighter jets, and precision-guided missiles.

Here, China’s monopoly is even more absolute. China controls not just the processing, but the vast majority of the global mining of heavy rare earths. In April 2025, Beijing flexed its geopolitical muscles by announcing sudden export restrictions on heavy rare earths, citing national security and domestic demand. The restriction sent Western defense contractors and automotive supply chains into an immediate panic, pausing production lines and exposing a catastrophic vulnerability.

In response, the West has turned its desperate gaze northward to one of the most hostile, yet strategically vital landmasses on Earth: Greenland.

Beneath Greenland's 1.7 million square kilometers of rapidly melting ice lies what geologists believe to be the largest unexploited concentration of rare earth minerals on the planet. The sudden global obsession with Greenland is not about climate research; it is a cutthroat race to secure a strategic choke point that could break China's rare earth monopoly for the next century.

Two specific deposits in Greenland have become the epicenter of this clash: Kvanefjeld and Tanbreez. The Kvanefjeld project has been mired in political controversy because its rare earths are mixed with radioactive uranium, leading to local mining bans. But just 30 miles away sits the Tanbreez deposit, which holds an estimated 28.2 million metric tons of rare earths, making it potentially the single largest deposit on Earth—larger than anything inside China.

The diplomatic bidding war over Tanbreez in 2025 was the stuff of espionage thrillers. Recognizing that a Chinese firm (Shenghe Resources) was already maneuvering to corner Greenland’s output, the US government intervened directly. In December 2025, American officials successfully lobbied the Tanbreez mine’s leadership to sell to a New York-based critical metals corporation. To sweeten the deal and lock out Chinese bidders, the US Export-Import Bank threw down a massive $120 million loan to finance the development—marking a historic, unprecedented US government investment in overseas mining.

Simultaneously, the European Union has designated Greenlandic graphite and rare earth projects as "strategic" under its Critical Raw Materials Act, desperate to secure its own slice of the Arctic pie. The ice of Greenland is melting, and underneath it lies the geopolitical leverage of tomorrow.

The Rise of Indonesia and the Quest for Alternatives

While the West looks to the Arctic for rare earths, the battery industry is looking to Southeast Asia to break the DRC's grip on cobalt and nickel. The undeniable rising star of the 2026 critical minerals market is Indonesia.

Historically a powerhouse in nickel mining, Indonesia has leveraged its vast resources to aggressively push into the cobalt space. They are achieving this not through traditional mining, but as a byproduct of processing low-grade nickel ore using a highly complex and capital-intensive technology called High-Pressure Acid Leaching (HPAL).

Billions of dollars in foreign direct investment—predominantly, and ironically, from Chinese battery giants like Tsingshan and CATL—have poured into Indonesian HPAL facilities. These plants use extreme heat, pressure, and sulfuric acid to extract both nickel and cobalt from laterite ores. The results have been spectacular. By 2025, Indonesia had skyrocketed to become the world's second-largest cobalt producer, capturing roughly 14.9% of the global market. By 2026, Indonesian cobalt output is projected to surge by another 21.2%, hitting nearly 60 kilotonnes.

However, Indonesia’s rise is not without severe economic and environmental complications. HPAL technology is incredibly carbon-intensive and produces millions of tons of highly toxic, acidic tailings (waste). The challenge of safely storing this toxic sludge in a tropical, seismically active archipelago prone to heavy rainfall is immense. If a tailings dam were to collapse, the ecological devastation would be catastrophic. Thus, while Indonesian cobalt helps ease the world's reliance on the DRC, it trades one set of severe ESG headaches (human rights and child labor) for another (toxic waste and deforestation).

The Circular Economy: Urban Mining and the Final Frontier

As the sheer economic cost and environmental damage of extracting raw materials become increasingly unsustainable, the most lucrative "mine" of the future will not be in the Congo, Indonesia, or Greenland. It will be in the world's junkyards.

By 2026, the first major wave of electric vehicles sold in the mid-2010s is reaching the end of its lifecycle. This has birthed a massive, rapidly scaling secondary industry: battery recycling, often referred to as "urban mining."

When lithium-ion batteries die, they are shredded into a granular, mineral-rich substance known in the industry as "black mass." This black mass contains highly concentrated amounts of lithium, nickel, and cobalt. Economically, extracting these metals from black mass is highly efficient. Recycled cobalt requires vastly less energy to process than virgin ore, carries zero human rights baggage, and dramatically reduces supply chain vulnerability. By 2026, secondary supply from recycling is the fastest-growing segment of the cobalt market, expanding at a projected CAGR of over 10%. Governments in the US and EU are heavily subsidizing domestic recycling infrastructure, viewing the millions of dead batteries within their borders as a strategic, sovereign asset that can be endlessly looped back into the supply chain.

Simultaneously, nations are looking downward to the final, most controversial frontier of resource extraction: deep-sea mining. Trillions of polymetallic nodules—potato-sized rocks rich in cobalt, nickel, copper, and manganese—litter the abyssal plains of the Pacific Ocean. While companies argue that vacuuming these nodules from the seafloor is cleaner than ripping up rainforests or relying on child labor, marine biologists warn of irreversible devastation to deeply fragile, undiscovered aquatic ecosystems. In 2026, deep-sea mining remains a fierce economic and legislative battleground, representing the ultimate ethical paradox of the green transition: destroying the earth to save it.

The Great Game of the Green Transition

The global transition away from fossil fuels was supposed to democratize energy, freeing the world from the volatile grips of petrostates and pipeline politics. Instead, it has simply shifted the board. We have traded drill rigs for open-pit mines, and oil barrels for battery cells.

As we progress through 2026 and look toward 2030, the economics of cobalt and rare earth minerals stand as the ultimate testament to human ingenuity and geopolitical ruthlessless. It is a market where the stroke of a pen in Kinshasa can double prices overnight; where a Chinese export ban can ground Western defense contractors; where the frozen shores of Greenland become the most coveted real estate on Earth; and where brilliant chemists work frantically in laboratories to render the whole violent game obsolete through LFP and sodium-ion innovations.

The cobalt rush is not just an economic phenomenon; it is a profound reordering of global power. The nations and corporations that can successfully navigate the price shocks, master the chemical processing, ethically source the raw dirt, and pioneer the recycling loops of tomorrow will not just dominate the critical minerals market. They will own the infrastructure of the 21st century.

Reference:

- https://www.mining-technology.com/analyst-comment/drc-indonesia-anchor-global-cobalt-supply/

- https://www.youtube.com/watch?app=desktop&v=2DetBTH26WU

- https://www.unsw.edu.au/newsroom/news/2026/02/blood-cobalt-disappearing-from-batteries-cheaper-cleaner-batteries-arriving

- https://www.grandviewresearch.com/industry-analysis/cobalt-market-report

- https://ima-api.org/cobalt-prices-will-likely-rise-in-2026-on-congos-export-quota/

- https://www.mordorintelligence.com/industry-reports/cobalt-market

- https://www.ecofinagency.com/news-industry/0201-51737-drc-extends-use-of-2025-cobalt-export-quotas-to-end-march-2026

- https://moderndiplomacy.eu/2026/02/25/congos-cobalt-curbs-expose-chinas-critical-metals-vulnerability/

- https://www.sapeople.com/opinion/global-south-dead-drc-mineral-deal/

- https://insideevs.com/news/784963/lfp-overtakes-nickel-battery-chemistry/

- https://farmonaut.com/mining/cobalt-glencore-2026-outlook-for-glencore-cobalt-mine

- https://evinfo.net/2026/01/lfp-became-the-dominant-ev-battery-chemistry-in-2025/

- https://addionics.com/blog/step-aside-nickel-and-cobalt-lfp-is-on-the-market-and-is-here-to-stay/

- https://www.batterytechonline.com/materials/7-most-hyped-battery-chemistries-in-2025

- https://chemaf.com/global-cobalt-market-to-be-driven-by-the-rising-application-of-cobalt-in-various-end-use-industries-in-the-forecast-period-of-2022-2027/